City of Hartford Treasurer Adam Cloud is scheduled to meet with the Council’s Operations, Management, Budget, and Government Accountability Committee on the evening of Monday, May 2, 2016.

The Office of the Treasurer acts as a co-issuer of the City’s debt and as the investor of the pension fund. Both the debt and the pension contributions have been cited as contributing factors to Hartford’s structural budget deficit.

As City leaders work to restructure Hartford’s finances, both closing this year’s budget gap and putting the City on a more sustainable long-term path, difficult questions need to be asked. Nothing should be exempt from scrutiny.

The Treasurer’s appearance at the Committee meeting is a rare opportunity for the community, via its Council members, to ask important questions of the Treasurer.

Questions About the General Obligation Debt

Treasurer Cloud, you have appeared before previous Councils to advocate for numerous general obligation bond sales. Some sales have been new debt to fund capital projects, while others have been restructurings of the existing debt.

We’re now being told that the City has too much general obligation debt, and that the worst is yet to come in terms of repayment.

Do you believe Hartford has too much general obligation debt? If yes, why haven’t you sounded the alarm in the same way that you have about potential decreases in pension contributions? If no, what metrics do you use to gauge the appropriate level of debt?

What do you recommend Hartford do with respect to managing the debt?

Questions About the Pension Fund

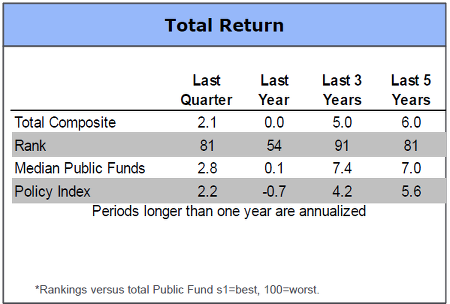

The Fourth Quarter 2015 Investment Performance Analysis report for the Municipal Employees’ Retirement Fund (MERF) stated that investment performance has been very poor over the past 5 years. The MERF’s total return was worse than 80% of the other public funds in the benchmark.

Specifically, the MERF’s return is reported as 1% behind the median fund over 5 years. The underperformance has cost the MERF an estimated $10 million per year (1% of a $1 billion fund), or $50 million over five years.

Why is the MERF ranked near the bottom of Public Funds for long term investment returns?

What have you done, and what are you planning to do, to improve performance?