Hartford’s leaders passed a balanced budget for fiscal 2016.

Reports varied about the precise size of the budget gap leaders overcame. The Committee on the Restructuring of City Government reported the gap to be $40.4 million at their first meeting in January. The Mayor’s Message that accompanied the adopted budget noted that leadership mitigated a $48.7 million budget gap. The official press release on May 28th characterized the gap as “more than $40 million.”

Regardless of the exact figure, three primary strategies were used to bridge the majority of the $40+ million gap.

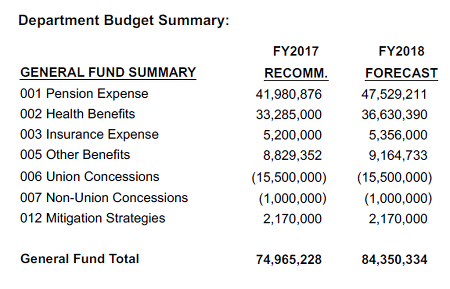

First, “sustainable department cuts” were made that saved $12.8 million. The description that accompanied the dollar figure noted that there would be no cuts in “essential” services. The savings came via increased efficiency and, by implication, cuts to unnamed non-essential services.

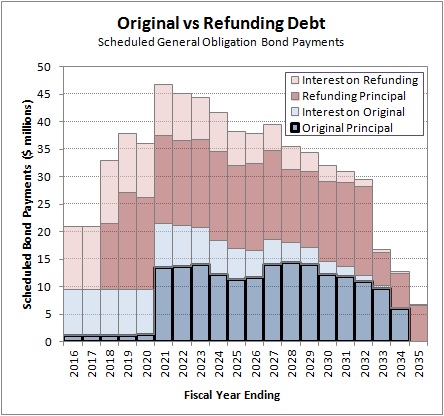

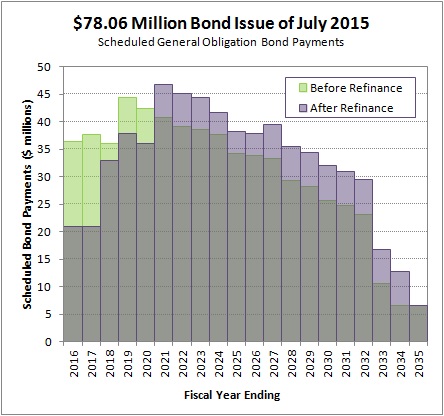

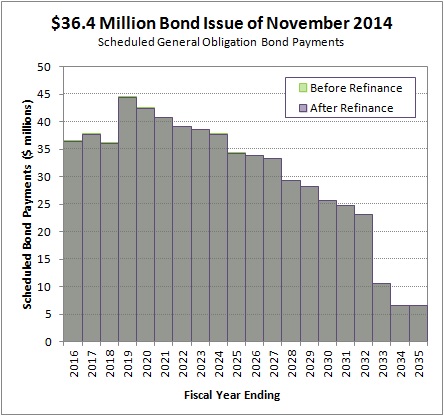

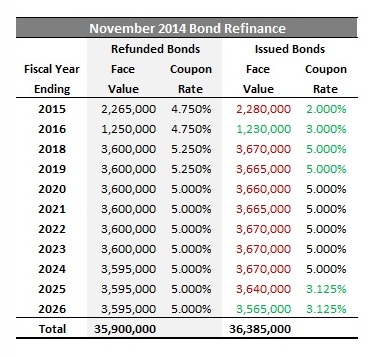

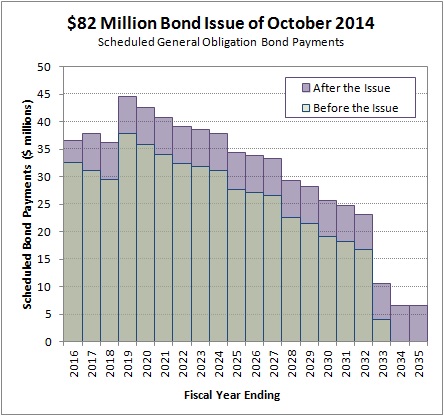

Next, the debt was restructured to reduce payments in fiscal 2016 by $12 million. The action was described as the “second phase” of debt restructurings, and it was noted that leadership planned to “gradually increase our existing debt service over the next five years.”

Finally, the City negotiated a deal with the Schools to spend $13 million that had been set aside by the Board of Education. The details of the agreement are not posted on the City’s website with the adopted budget. However, media reports have stated that in exchange for spending the $13 million, the City took on $11 million of school expenses in the capital improvement budget.

This year’s strategies did not include any efforts to address the structural nature of the budget gap.

Instead, the three primary strategies responsible for balancing the 2016 budget are likely to make the structural budget deficit worse in future years.

A recent police staffing report stated that the department is significantly understaffed. The police department is one of the “essential” public safety functions, raising immediate questions about whether department cuts are “sustainable.” The City has begun adding staff to backfill cuts made in this, and previous, budget cycles.

Restructuring the debt to reduce payments in fiscal 2016 and fiscal 2017 increased the payments in the future. Over the next two years Hartford is scheduled to pay off $2.24 million of the $424.9 million the City currently owes. The total owed will increase in coming years. The 2016 – 2020 Capital Improvement Plan that was approved in conjunction with the 2016 budget calls for over $378 million in net borrowing over the plan’s five year life (see page 17).

If media reports about the deal with the Schools to spend money earmarked for post employment benefits are accurate, then effect is two-fold. Taking the $13 million reduced the funding status of the Schools’ benefits program. The $11 million in future debt/payments the City accepted from the Schools repays some value, but doesn’t make the Schools whole. The Schools still have to rebuild the account balance, and they lose out on all the potential investment income that the $13 million would have generated.

On the City side, the $11 million the City added to the Capital Improvement Plan in exchange for access to the $13 million represents additional future costs too. The practical result was that the City borrowed $13 million to spend on this year’s operating expenses, and will repay it over time. One could argue that getting $13 million and repaying $11 million over time is a good deal. For some people, companies, or municipalities, a negative interest rate loan like that would be a good deal (it’s an arbitrage opportunity). For others, those that repeatedly restructure their debt to postpone repayment, borrowing to meet current operating expenses has a negative overall impact. It increased Hartford’s debt burden and decreased Hartford’s financial flexibility.

All three of the primary budget “balancing” strategies involved manipulating expenses to make the 2016 income, expenses, and cash flow work. None of the three strategies will help put Hartford on a more sustainable financial path, and each one is much more likely to make the structural budget gap worse.